The AI Transformation Imperative: What I Saw Inside the Buildings Everyone Talks About

By Jessie Kim · Johns Hopkins Carey Business School · Seattle Tech Trek, January 6–8, 2026

Firsthand Site Visits: AMAZON/AWS · PFIZER · ADOBE · MICROSOFT

In January 2026, I joined an alumni tech trek in Seattle with Johns Hopkins Carey Business School alum— spending three days inside the headquarters of Amazon, Pfizer, Adobe, and Microsoft, sitting across from senior leaders and graduated alum who were so proud to share their career success stories. I went in as a strategist with one question: underneath the headlines about AI transformation, what is actually happening inside these organizations — and what separates the ones capturing real value from the ones generating press releases?

We are past the point of asking whether artificial intelligence will transform enterprise business. The more pressing question — the one every board, every CFO, and every strategy team is sitting with right now — is whether the capital being deployed is actually generating the returns being claimed. And that question does not get easier when you read the headlines, because the headlines are contradicting each other.

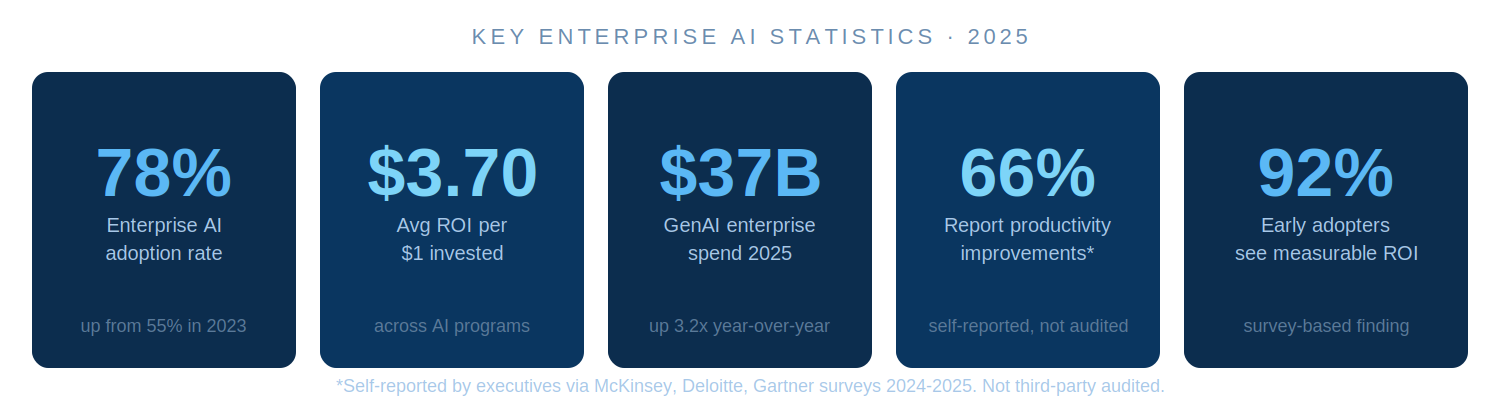

On one side: AI adoption has reached 78% of enterprises, companies are self-reporting productivity gains of 26–55%, and global enterprise GenAI spend hit $37 billion in 2025 — a 3.2× increase in a single year. On the other: Goldman Sachs' own economists published a report asking where the economy-wide productivity gains are. MIT economist Daron Acemoglu has estimated that AI will automate a fraction of what markets are pricing in. And 42% of companies abandoned most of their AI projects in 2025 — up from just 17% the year prior (we just never hear of these).

Both are true. The question is how to hold them at the same time — and what to do with that tension if you are advising organizations on where to invest.

Walking into Amazon, Pfizer, Adobe, and Microsoft in January gave me something that research alone cannot: a ground-level read on how AI transformation actually feels from the inside of organizations that are navigating it in real time. What I came back with is a clearer framework for why some enterprises are capturing genuine value and others are funding expensive experiments that will never reach a financial statement.

Note: Statistics are sourced from McKinsey, Deloitte, and Gartner annual surveys (2024–2025), and from Snowflake and Menlo Ventures research. Figures are self-reported by executives, managers, and IT leaders — they have not been independently audited or verified by third parties.

"Productivity gains" refers to self-reported improvements in task speed, output volume per employee, or process cycle time reduction — not changes to revenue, net margin, or audited financial performance. A productivity gain does not automatically translate to profit improvement; that only happens when freed capacity is redeployed into revenue-generating work or reflected in real headcount decisions. The broader debate on whether enterprise AI capital expenditure is generating economy-wide returns remains active among leading economists and analysts.

The ROI Tension Worth Naming Upfront

Before getting into what I observed on the ground, there is a mechanism worth understanding — one that explains why you can have genuine productivity gains and flat financial statements at the same time.

When a company reports a "20% productivity gain" from AI, they typically mean a specific team completes tasks faster. But if the business didn't reduce headcount, didn't redeploy those people into revenue-generating work, and wasn't previously bottlenecked by that team — the income statement looks identical. Same revenue. Same costs. Same profit. The productivity gain stayed inside the team and never reached the financial statements.

For a productivity gain to show up financially, one of three things has to happen: headcount is reduced, or the freed capacity is absorbed by growth, or the team was a genuine bottleneck preventing revenue.

The first — headcount reduction — is happening more than companies publicly advertise. The AI layoffs of 2024 and 2025 are, in many cases, exactly this mechanism playing out: productivity gains converted into cost savings by simply employing fewer people. What is less common, and far harder to execute, is the second and third scenario — where freed capacity gets redeployed into something that grows revenue rather than just cuts cost. That distinction matters enormously for how you evaluate whether an organization's AI strategy is building long-term value or simply shrinking its way to a better margin.

The enterprises I visited understand this distinction. The best of them have built their AI strategy around it.

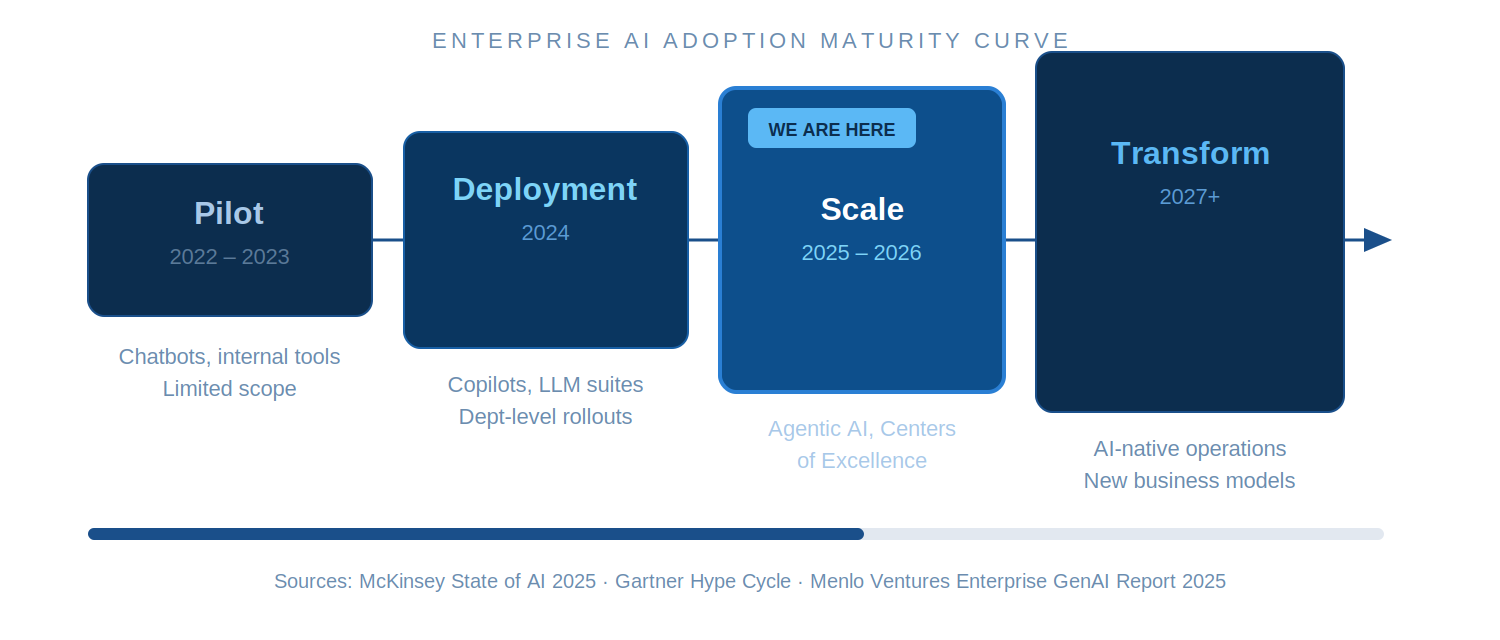

From Pilot to Production at Scale

The industry-wide AI adoption curve over the last four years maps cleanly onto what I saw across the three days of site visits. Most large organizations spent 2022 and 2023 in controlled experimentation — internal chatbots, document summarization, isolated proof-of-concepts. By 2024 the dam broke, and enterprise-wide deployments became the expectation rather than the exception. In 2025, the focus shifted to agentic AI — systems capable of completing complex, multi-step tasks autonomously. Every technology leader I spoke with across all four companies confirmed this trajectory without me prompting it.

Where enterprise AI spend is concentrating tells its own story. Coding represents 55% of all departmental AI spend — the single largest application category across the enterprise landscape, followed by IT operations, marketing, and customer success. That dominance is not a surprise to anyone who has spent time inside a technology organization. AI is first and foremost an internal productivity revolution, not a customer-facing one. The customer-facing returns come later, if at all, and only if the internal productivity is redirected into something that matters.

Note: Interpreting numbers, e.g. What the 10% actually meant in the chart

That number wasn't "10% of IT budget goes to AI." It was 10% of generative AI departmental spend goes to the IT function — meaning out of all the money companies are spending on GenAI tools across departments, IT as a department claims about 10% of that pie. Coding/engineering claimed 55%, which is why IT looks small by comparison.

Amazon & AWS: The Discipline to Let Things Die

Amazon Spheres · AWS Skills Center, Seattle · January 6, 2026 · CLOUD & RETAIL

We started at the Amazon Spheres — an iconic structure housing 40,000 plants from over 30 countries in the middle of downtown Seattle — before walking to the AWS Skills Center for a four-hour session that included a generative AI course, a panel, and direct time with a recruiter. The panelists were Johns Hopkins Carey alumni spanning finance, product marketing, and solutions architecture, each having used the same MBA foundation to build careers across different functions inside one of the most AI-forward companies in the world. What Amazon calls "being curious" is not a tagline. It is the operating culture — and you feel it in how people talk about building, testing, and yes, shutting things down to optimize for performance in business functions that are succeeding over others.

The insight that stayed with me from Amazon is not a product or a platform. It is their relationship with failure — and specifically, the organizational discipline to let things die when the data says to.

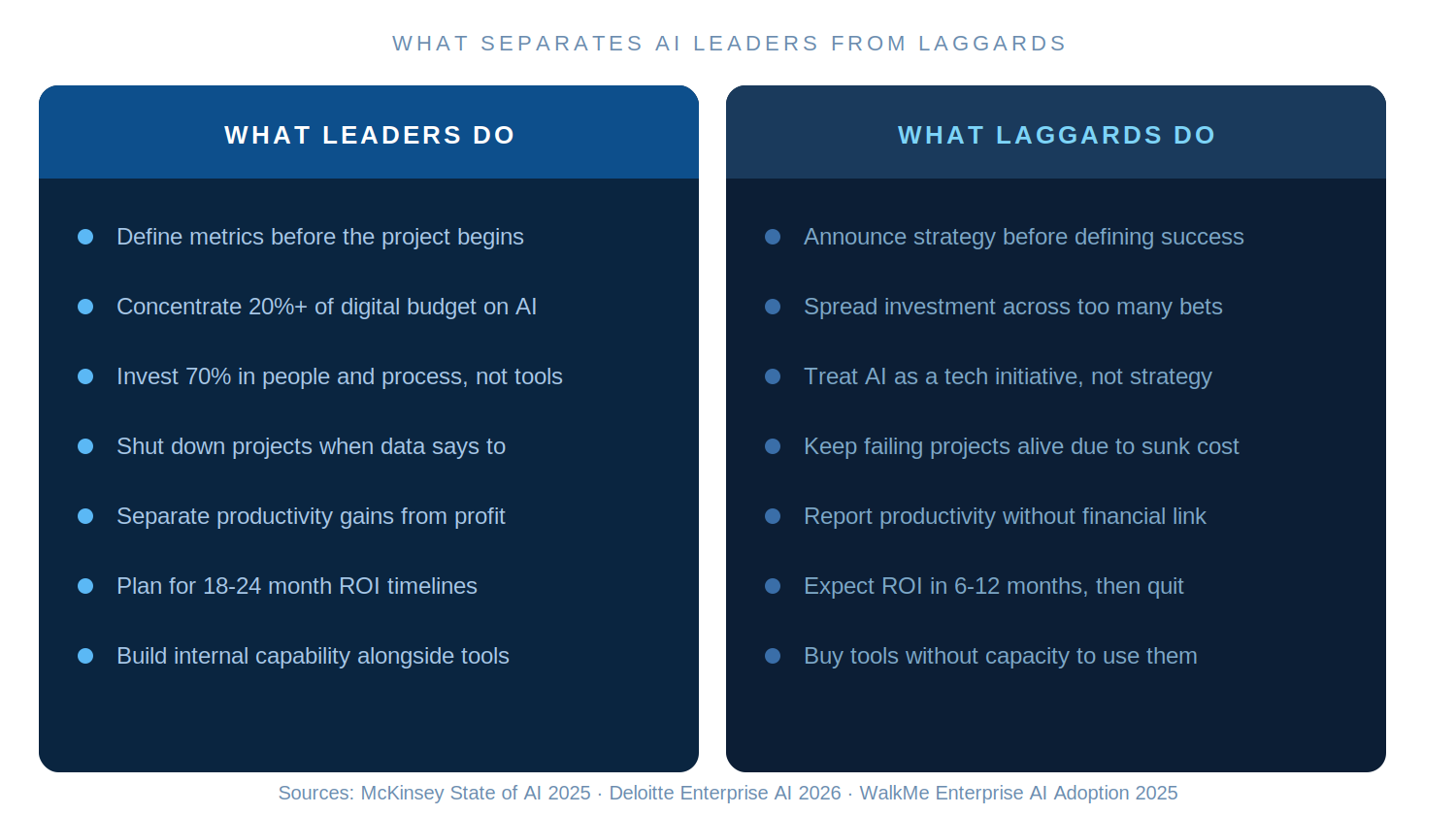

"The culture I observed is built around defining clear metrics and KPIs before a project begins — and being willing to follow the data wherever it leads, even if it leads to a shutdown. That kind of organizational discipline is rarer than it sounds."

Amazon Go was a flagship, highly public innovation. Cashierless retail, heavily covered by the press, seen by many as the future of shopping. During COVID, demand was exactly what Amazon had anticipated. And then, two years later, the data showed that demand had not sustained. So Amazon shut most of it down. Only a handful of locations remain, primarily serving employees on campus. An alumnus who had worked on that team shared this story openly, without embarrassment. Because at Amazon, that is not a failure story. That is a data story.

This is the counter-model to what most enterprises are doing with AI right now. Most organizations are afraid to kill AI projects because of optics, executive sponsorship, or sunk cost. The 42% abandonment rate I cited above represents companies finally shutting things down — but often after spending years and significant capital proving they never should have started in the first place. Amazon's posture is different: the question is never "did we build something cool?" It is always "did the data justify keeping it?"

That discipline — defining what success looks like before the project begins, maintaining consensus around those measures throughout, and being willing to act on the results — is precisely what separates organizations capturing real AI value from those funding expensive experiments. It is the single most important capability an enterprise can build as it deploys AI at scale, and it is the hardest to sustain when leadership is eager to declare transformation.

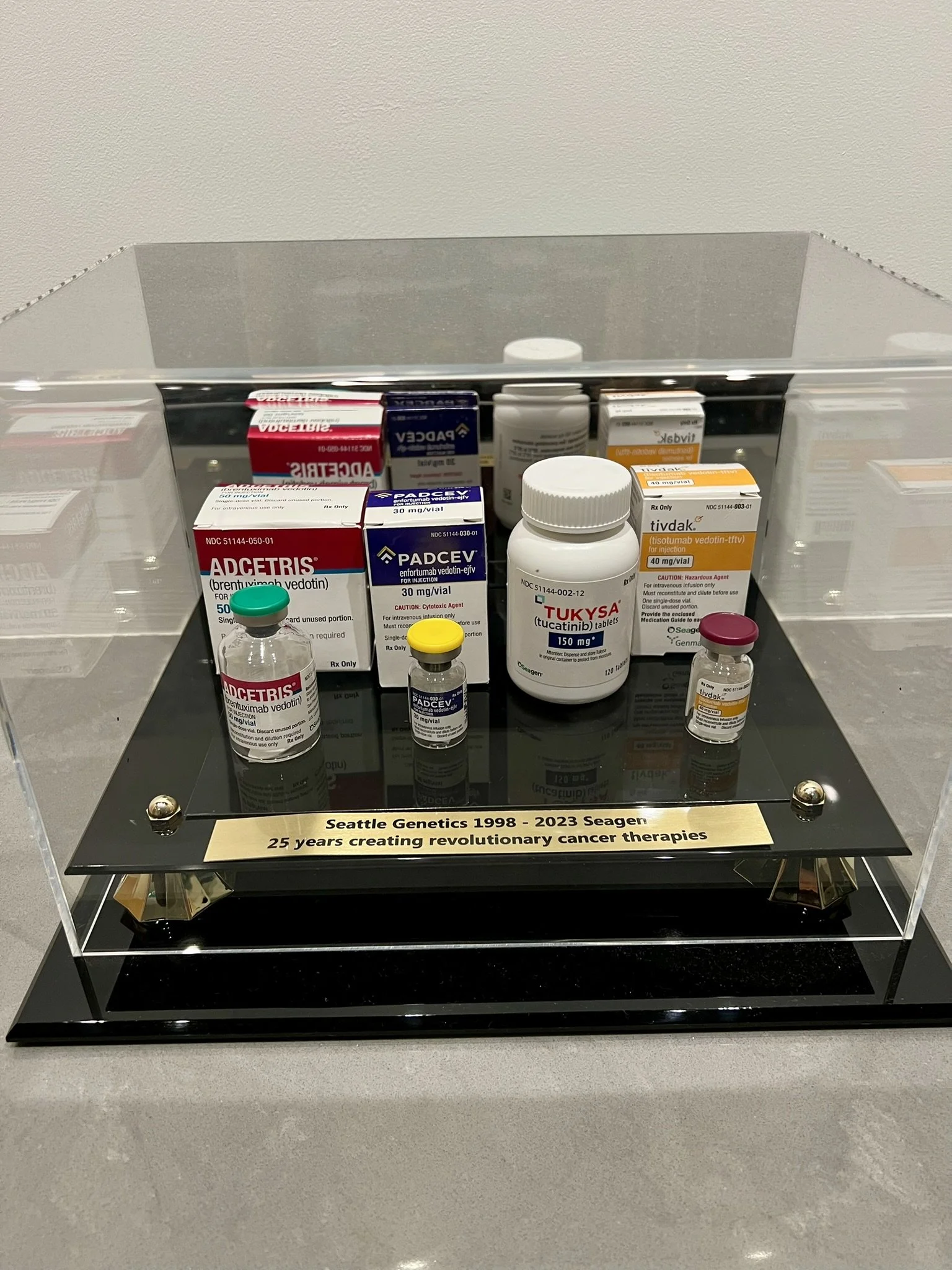

Pfizer: Compressing Drug Discovery Timelines — With the Right Constraints

Pfizer R&D Labs, Bothell, WA · January 7, 2026 · PHARMA & BIOTECH

Pfizer's Pacific Northwest presence in Bothell, Washington is a direct result of their Seagen acquisition, which significantly expanded their oncology footprint in the region. I put on a white coat and walked through their mRNA R&D labs, watching scientists work with the actual machinery of drug development: bioprocessing equipment, upstream production pipelines, and the extraction of proteins from Chinese Hamster ovary cells — the industry-standard biological substrate for vaccine and antibody development. (We were not allowed to record.) That restriction alone tells you something about how proprietary and serious the real science is. Five senior leaders joined a panel afterward: John Sourke, VP of Global Operations based in Ireland who remote dialed in, Kate Ostbye, Senior Director of R&D Data Science & Machine Learning, who leads a team of engineers and ML practitioners; Jeremy Shaver, PhD, Senior Director of ML & Data Analytics, Ryan Take, warehouse site head of manufacturing overseeing seamless production from Bothell to Ireland, and Corinna Palanca-Wessels, MD PhD, Executive Medical Director overseeing oncology strategy across early and late-stage development.

The numbers from Pfizer's AI programs are genuinely significant. Their collaboration with AWS — focused on AI-powered research data infrastructure for 1,500 scientists — delivered an 80% reduction in data discovery time, saving over 16,000 hours of manual search annually. A single drug development effort can generate approximately 20,000 documents. Before AI, scientists navigated those manually across multiple tools. The time compression is real, and so is the cost reduction: infrastructure costs dropped 55%. Their mRNA AI algorithm delivered 20,000 additional vaccine doses per batch — a meaningful capacity gain at population scale.

"The Senior Director with the MD/PhD said it plainly: risk means something different here. Public safety is in the balance. Data integrity, safety, and quality come before speed — and that is not a constraint on AI strategy. It is the governing framework."

But here is what the press release cannot tell you: standing in that building, talking to those leaders, I understood something about how Pfizer evaluates AI ROI that is entirely different from every other industry I have worked in or studied.

If they are developing an antibody drug, every AI-assisted decision must account for what happens to a human being at scale. The ROI question is not "did this save money?" It is "did this make the science more accurate, safer, and better for patients?" Revenue follows from that — and the executive medical director, Dr. Palanca-Wessels, was explicit in stating that helping patients is the strategy, not a byproduct of it. That inverted revenue model changes everything about how AI value is measured in life sciences.

Their AI Center of Excellence is real and active. Their focus for 2026 is specifically agentic AI — autonomous systems capable of handling complex, multi-step research tasks — which is exactly in line with where the broader industry is heading. They have built proprietary internal AI infrastructure, operate on a hybrid model, and their governing constraint on everything they build is data privacy. That is not a limitation. It is what makes the science trustworthy.

The most powerful moment of the three-day trek came when someone asked the VP from Ireland how Pfizer made it through COVID. He described an organizational moment that I think about differently now than I would have before walking into that building. Pfizer's entire operating philosophy is built around quality over speed — and COVID forced them to achieve both simultaneously, at a scale and on a timeline that had never been done in the history of pharmaceutical development. He was visibly proud, and immediately clear-eyed: that was an emergency. An exception. External pressure to operate at that pace permanently is something he pushes back on firmly. That was a moment of unprecedented resilience. It cannot become the new baseline.

I walked down those hallways and felt the culture in a way I did not expect. Every single leader who spoke had genuine values. A continuously improving culture was not a talking point — it was simply how they think. That is not something you get from a case study.

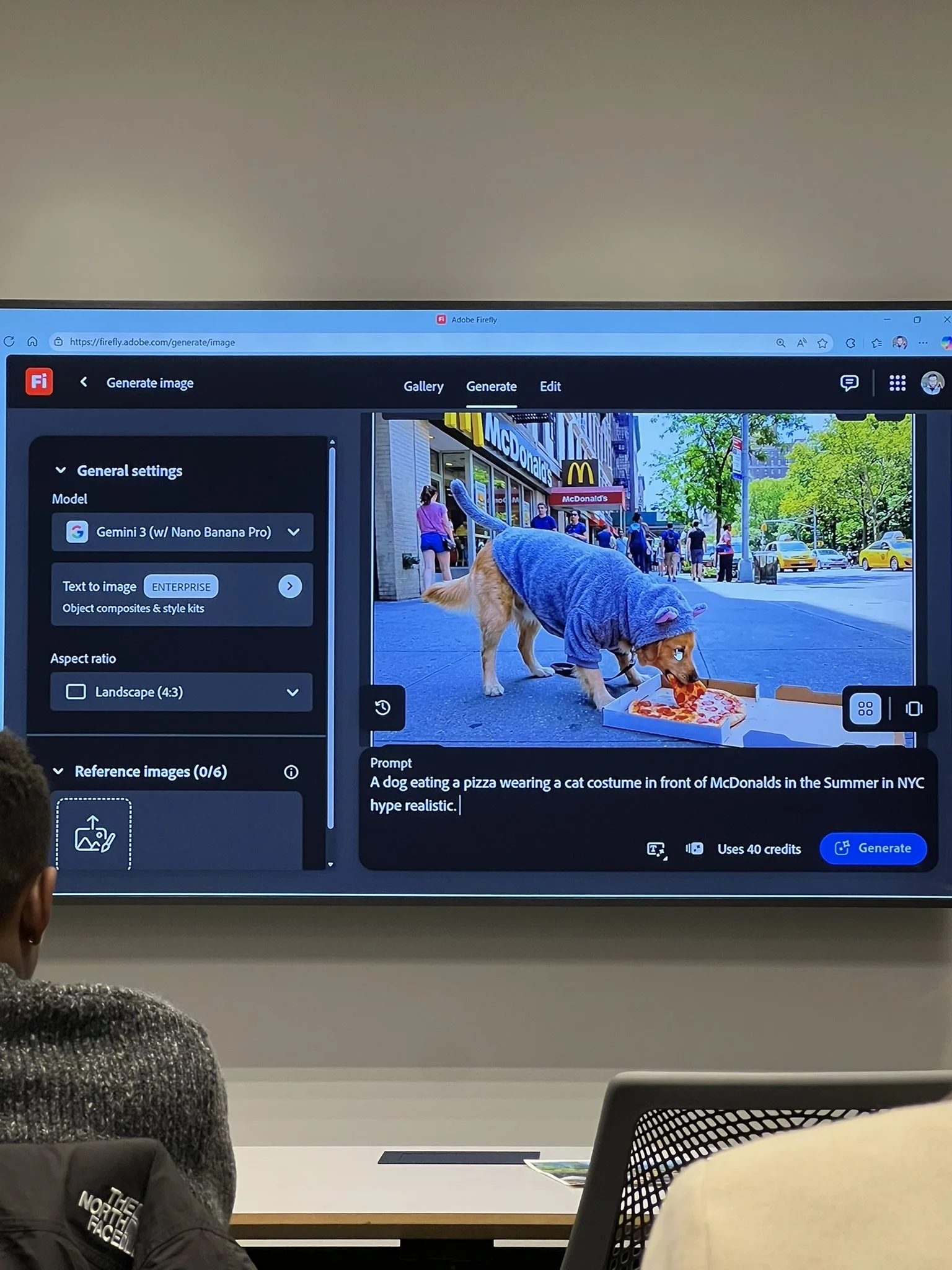

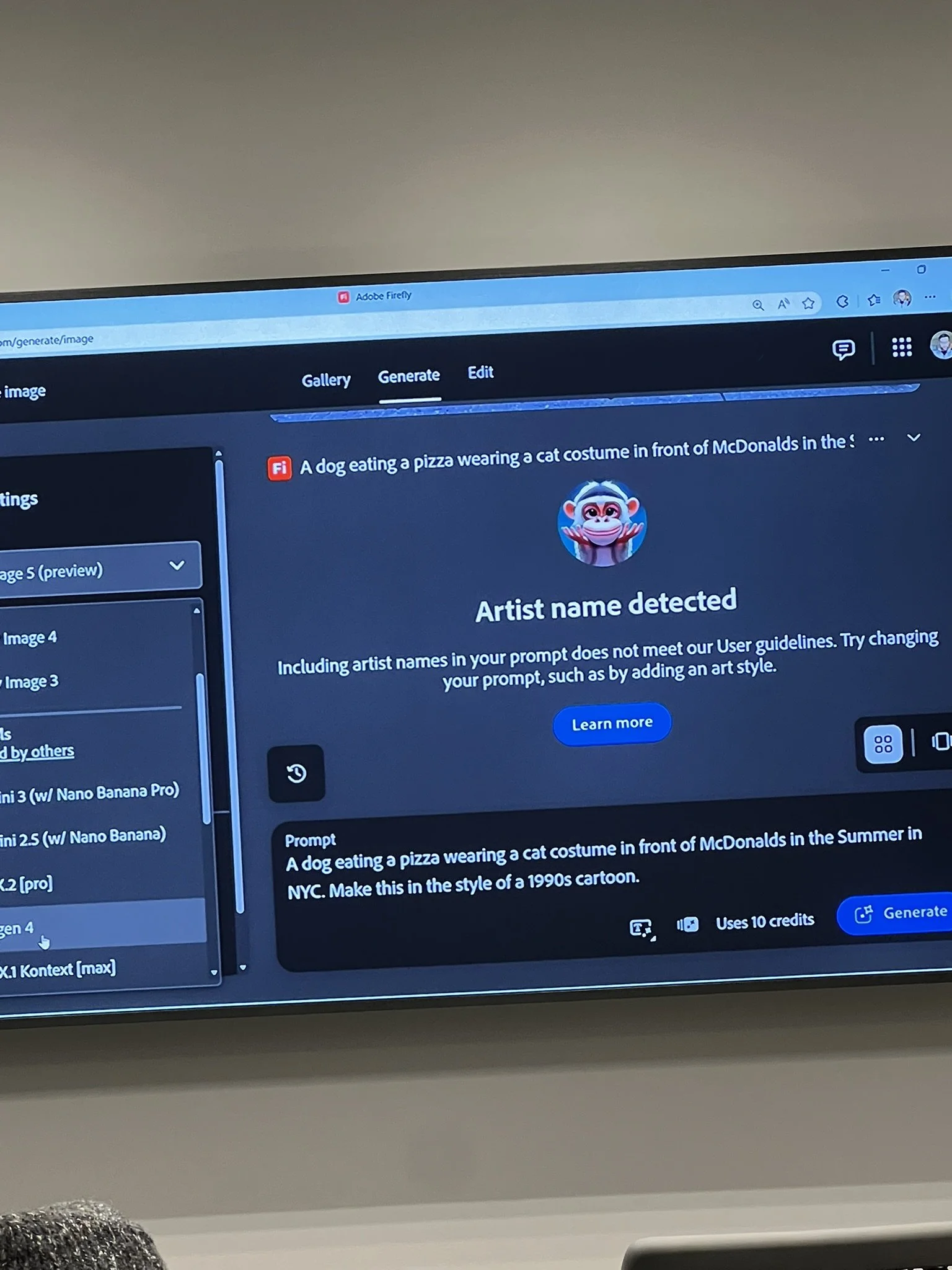

Adobe: Defending Creative Value When the Ground Is Shifting

Adobe Seattle, Fremont / South Lake Union · January 7, 2026 · CREATIVE SOFTWARE

Adobe sees itself as the creative branch of Microsoft — and that association is not accidental. The strategic logic is clear: Microsoft owns the productivity layer of enterprise software, and Adobe wants to own the creative layer. The challenge is that the creative software market is being disrupted from every direction simultaneously, with new GenAI tools launching constantly, many of them free.

"Adobe's strategic moat is integration depth. AI is embedded across every Creative Cloud app, inside Acrobat, throughout the entire ecosystem. Whether that holds against free tools and nimble startups is the open question — and the pressure in that room was palpable."

The centerpiece of the Adobe visit was a live demo of Firefly, their generative AI platform, and the philosophy behind it is worth understanding as a strategic position. The insight was not simply "we have a GenAI tool." It was a pointed observation about how creative professionals actually work: they should not have to have ChatGPT open in one tab, Gemini in another, a video tool running somewhere else, and a separate image generator alongside. Firefly consolidates generation, editing, and video into one integrated creative interface. The bet is that workflow coherence — keeping a creative professional in flow rather than fragmenting their attention across a dozen tools — will be more valuable than any single capability.

The honest competitive challenge is real: the market for AI-powered creative tools is expanding in every direction, and price compression is relentless. Adobe's answer — deeper integration, more seamless workflow, AI as an embedded layer rather than a bolt-on feature — is a coherent strategic response. But it comes with a monetization tension: many of the most compelling AI features require a higher subscription tier, which creates friction with the very users Adobe needs to retain. That is a strategic risk worth watching.

What I walked away believing is that Adobe's culture — genuinely warm, inclusive, built around creativity as a core organizational value — is itself a form of competitive advantage when it comes to attracting and retaining the people who build those products. That music room is not decoration. It is a signal.

Microsoft: The Defining Bet — and What It Looks Like From Inside

Microsoft East Campus, Redmond WA · January 8, 2026 · ENTERPRISE TECHNOLOGY

Microsoft's campus in Redmond feels like a city. We spent six hours there and still did not see all of it. The food court felt like an airport — vast, clean, dozens of restaurants. And rolling through the campus perimeter was a white autonomous security robot on wheels, cameras extending from every side, continuously scanning its environment. It was a small but telling detail: the AI capital at Microsoft is not just in the products. It is embedded in how they run the building itself. We heard from three leaders: Danielle Crayton from Commercial Cloud & AI (Sr. Director, Azure SMB), Tammy Ibeama, Product Marketing Manager on the Copilot AI team, and an engineering from Microsoft Research Health Futures, who leads Health & Life Sciences Strategy and Partnerships with a focus on AI in healthcare and precision medicine.

No enterprise software company has staked more on AI transformation than Microsoft — and the numbers are beginning to validate the wager. Microsoft's AI business has reached a $37 billion annualized revenue run rate, meaning current quarterly AI revenue projected forward at today's pace over a full year — growing over 120% year-over-year. Copilot now has 20 million seats, the fastest pace of net additions since the product launched. Vodafone employees are saving an average of three hours per week — reclaiming 10% of their working week. Lumen Technologies estimates $50 million in annual savings. A Forrester study found organizations adopting Microsoft 365 Copilot can expect a projected three-year ROI ranging from 112% to 457%.

What is important to understand about Microsoft's bet is that it is not a feature strategy. It is an identity strategy. AI is not something Microsoft added to its products. AI has become what Microsoft is — woven into the daily tools that knowledge workers already use, compounding as adoption deepens. Every person I spoke with on that campus, regardless of role or seniority, thinks at scale from the first moment of any conversation. Whatever they build has to work for millions of users. That is not an afterthought. It is the starting assumption, and it shapes every product and every partnership decision they make.

"Danielle said she loves to solve messy problems. That landed for me personally — because I feel the same way. The leaders I most respected in that building were not the ones with the most polished answers. They were the ones most comfortable operating in ambiguity, who humbly displayed curiosity, and generated ideas of new possibilities anyway."

Danielle Crayton, Sr. Director of Azure SMB marketing and holds an MBA from McComb School of Business, reinforced something I want to carry forward into my own consulting work: being an "idea person" — someone who constantly generates possibilities, proposes solutions, and moves toward complexity rather than away from it — is what makes a leader. If you can bring new ideas to a problem, you bring value. That is a deceptively simple statement with real strategic weight.

The Health and Life Sciences team confirmed what the industry data shows: engineers are using AI heavily for coding, which currently represents 55% of all enterprise AI departmental spend. The team’s work at the intersection of AI, healthcare, and precision medicine points toward where Microsoft's next wave of value creation is aimed — not just productivity inside enterprises, but accelerating scientific discovery across sectors, which is exactly the space Pfizer is navigating from the other side.

One unexpected cultural-talent insight: Microsoft employees in marketing and commercial roles are actively encouraged to build and maintain LinkedIn presence — not as a casual suggestion but as a cultural norm. The reason is structurally elegant. Microsoft owns LinkedIn. Their employees building personal brand on that platform are simultaneously serving the product's growth ecosystem. It is a quiet but deliberate alignment of personal and corporate strategy that most companies never achieve.

What Separates Leaders from Laggards

The enthusiasm is real, but so is the execution gap. As noted earlier, 70–85% of AI projects still fail, and 42% of companies abandoned most of their AI projects in 2025 — often citing cost overruns and unclear value as the primary reasons. Revenue growth from AI largely remains an aspiration: 74% of organizations hope to grow revenue through AI in the future, compared to just 20% that are already doing so.

Johnson & Johnson's experience is instructive. With nearly 900 generative AI projects running, they found that just 10–15% of those projects delivered 80% of the value. They have since concentrated investment in high-impact areas: drug discovery and supply chain optimization. That discipline — knowing where to focus rather than spreading AI investment across every possible surface — is itself a form of competitive advantage.

The through-line across all four companies I visited is consistent with this framework. Amazon has made data the final authority on what lives and what dies. Pfizer has built quality and patient outcomes as the governing constraint on AI investment. Adobe is concentrating on integration depth rather than feature breadth. Microsoft has bet the entire company identity on AI at enterprise scale. None of them are doing everything at once. All of them have a clear point of view on where the value is — and are organizing around it.

The Road Ahead

Gartner predicts that by 2028, 33% of enterprise software will include agentic AI — autonomous systems capable of handling complex tasks and making decisions — up from less than 1% in 2024. That shift from assistive AI to agentic AI will demand a different organizational posture: stronger governance, clearer human escalation paths, and a fundamental rethinking of how workflows are structured. Every technology leader I spoke with across the trek mentioned agentic AI as their primary 2026 focus area. Pfizer's Center of Excellence named it explicitly. This is not a future trend — it is an active deployment decision happening right now inside these organizations.

Now Concentration and discipline. The enterprises capturing value are those who have stopped treating AI as a portfolio of experiments and started treating it as a core business strategy with defined metrics, concentrated investment, and the organizational willingness to act on what the data shows.

2027 Agentic AI at scale. Autonomous systems handling multi-step workflows — in drug discovery, in enterprise software, in creative production — will move from pilot to production. The governance frameworks for human oversight are being built now and will determine who scales safely and who creates liability.

2028+ AI-native business models. The organizations that will look unrecognizable in five years are not the ones adding AI to existing operations. They are the ones using AI to build entirely new operating structures — where the question is not "how do we make this process faster" but "does this process need to exist at all."

The stocks doing well reflect investor faith in that long-term thesis. The ROI debate is about whether that faith is being earned fast enough — and whether the companies spending $37 billion a year on AI infrastructure will ever see it in their income statements. That gap between faith and evidence is where good consultants live.

I came back from Seattle more convinced of that than ever — and with a sharper sense of what it actually looks like when an organization is doing this right. It does not look like a press release. It looks like a team that defined their metrics before they started, a leader who pushes back on external pressure to sacrifice quality for speed, and a culture that is willing to close down Amazon Go when the data says to.

That is the standard. And most organizations are not there yet.

References

Armitage, H. (2025, June 5). Clinicians can 'chat' with medical records through new AI software, ChatEHR. Stanford Medicine News Center. https://med.stanford.edu/news/all-news/2025/06/chatehr.html

Deloitte. (2026). The state of AI in the enterprise. Deloitte Insights. https://www.deloitte.com/us/en/what-we-do/capabilities/applied-artificial-intelligence

Enterprise Strategy Group & Snowflake. (2025, April 15). Snowflake research reveals that 92% of early adopters see ROI from AI investments [Press release]. Snowflake. https://www.snowflake.com/en/news/press-releases

Fullview. (2026, March 31). 200+ AI statistics & trends for 2025: The ultimate roundup. https://www.fullview.io/blog/ai-statistics

Johns Hopkins Carey Business School. (2026). Seattle tech trek agenda, January 6–8, 2026 [Internal program document]. Johns Hopkins University.

Lucidate. (2025, July 22). Goldman Sachs scales AI coding to thousands of agents — 3x productivity gains expected. https://lucidate.substack.com/p/goldman-sachs-scales-ai-coding-to

McKinsey & Company. (2025). The state of AI 2025. McKinsey Global Institute.

Menlo Ventures. (2026, March 19). 2025: The state of generative AI in the enterprise. https://menlovc.com/perspective/2025-the-state-of-generative-ai-in-the-enterprise/

Microsoft Corporation. (2025, July 30). Microsoft cloud and AI strength fuels fourth quarter results [Form 8-K]. U.S. Securities and Exchange Commission. https://www.sec.gov/Archives/edgar/data/0000789019

Pfizer & Amazon Web Services. (2024). Driving patient-centric innovation in life sciences using generative AI with Pfizer [Case study]. AWS. https://aws.amazon.com/solutions/case-studies/pfizer-PACT-case-study/

WalkMe. (2025, November). The state of enterprise AI adoption in 2025. https://www.walkme.com/blog/enterprise-ai-adoption/